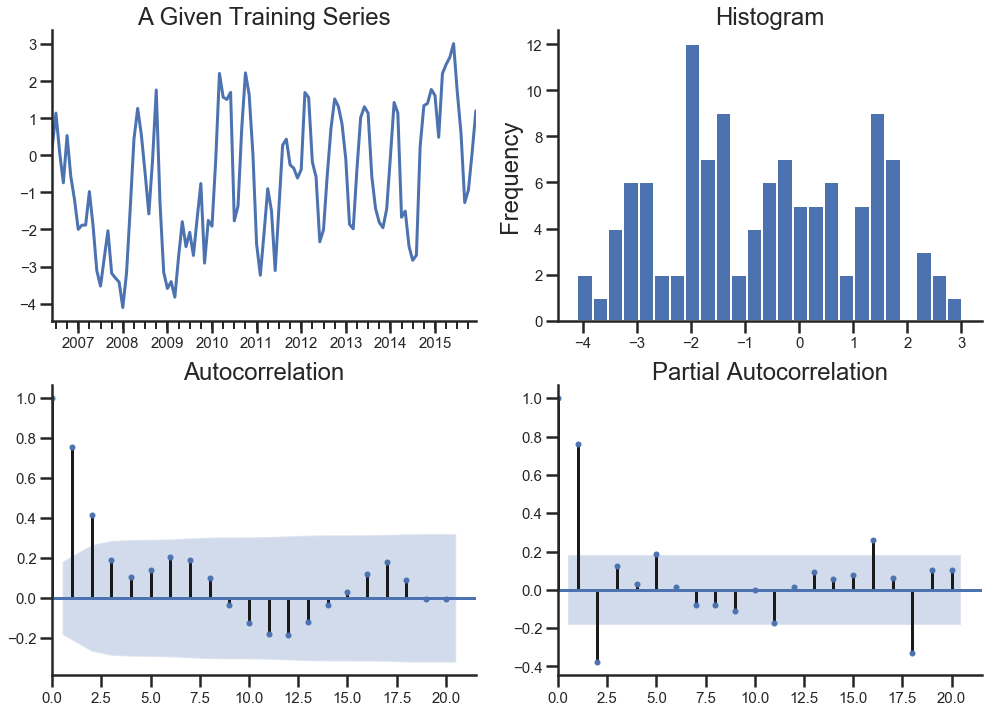

tsplot(ts_train, title='A Given Training Series', lags=20)

(<matplotlib.axes._subplots.AxesSubplot at 0x1c21cf6080>,

<matplotlib.axes._subplots.AxesSubplot at 0x1c2240c358>,

<matplotlib.axes._subplots.AxesSubplot at 0x1c22432e10>)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

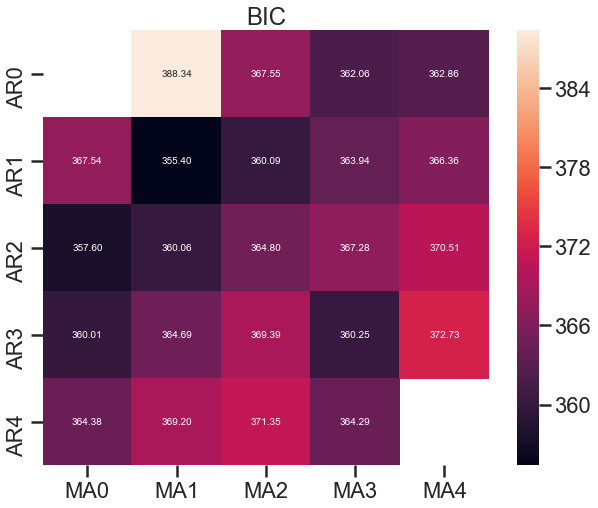

results_bic = pd.DataFrame(index=['AR{}'.format(i) for i inrange(p_min, p_max+1)], columns=['MA{}'.format(i) for i inrange(q_min, q_max+1)])

for p, d, q in itertools.product(range(p_min,p_max+1), range(d_min, d_max+1), range(q_min, q_max+1)): if p == 0and d==0and q==0: results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = np.nan continue try: model = sm.tsa.SARIMAX(ts_train, order=(p,d,q)) results = model.fit() results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = results.bic except: continue results_bic = results_bic[results_bic.columns].astype(float)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/statespace/sarimax.py:961: UserWarning: Non-invertible starting MA parameters found. Using zeros as starting parameters.

warn('Non-invertible starting MA parameters found.'

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/statespace/sarimax.py:949: UserWarning: Non-stationary starting autoregressive parameters found. Using zeros as starting parameters.

warn('Non-stationary starting autoregressive parameters'

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/base/model.py:512: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/base/model.py:512: ConvergenceWarning: Maximum Likelihood optimization failed to converge. Check mle_retvals

"Check mle_retvals", ConvergenceWarning)

//anaconda3/lib/python3.7/site-packages/statsmodels/tsa/base/tsa_model.py:165: ValueWarning: No frequency information was provided, so inferred frequency MS will be used.

% freq, ValueWarning)